Toward the endo of Deflation, focus on Okinawa, active ETFs, and Gigacast.

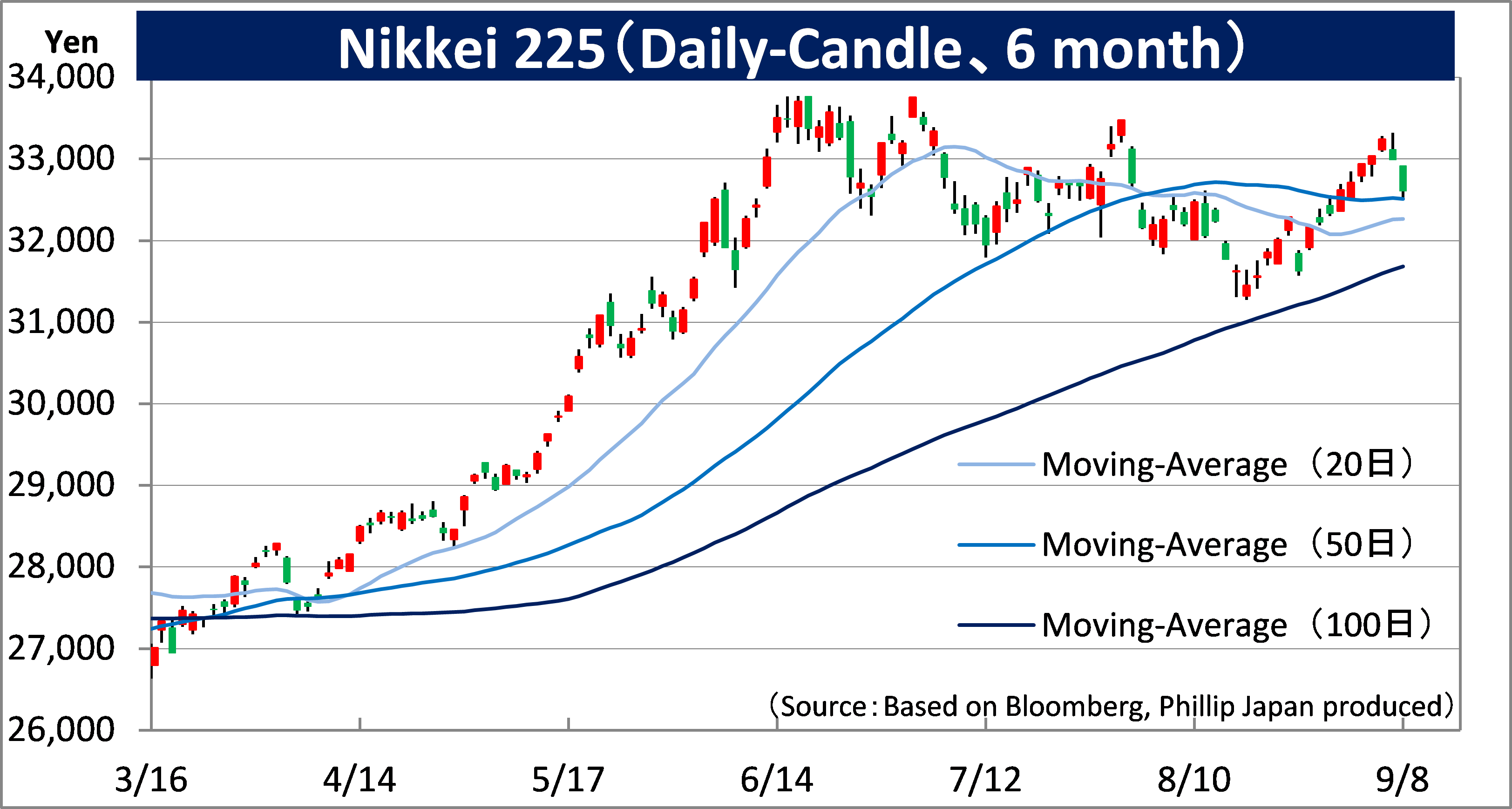

■The Cabinet Office on Thursday released an estimate that the supply-demand gap, which represents the difference between supply and demand in the Japanese economy, was plus 0.4% in April-June, the first time the demand deficit has been resolved in 15 quarters since the July-September period of 2019. Although the BOJ’s April-June estimate has not yet been released, it is possible that all four indicators that the government focuses on in ending deflation ((1) supply-demand gap, (2) CPI inflation more than 2% YoY, (3) GDP deflator, and (4) unit labor cost) were all positive. While Japan is getting closer to overcoming deflation, the monthly labor statistics for July released on September 7th indicated that real wages per capita, which take prices into account, fell 2.5% y/y for the 16th consecutive month of negative growth. The decline also expanded from 1.6% in June, indicating the need for further engine acceleration toward the main goal of overcoming deflation.

■Among banking stocks, regional bank stocks, whose share prices are less well positioned from their 2015 highs compared to megabanks, remain in focus for the monetary easing correction that will accompany the end of deflation. We featured Hokkaido-based Hokuhoku Financial G (8377) in last week’s issue of this Weekly’s “Pick Up” issue. In other regions, Okinawa is particularly noteworthy. While people say that “Japan is a country of declining population and lacks investment opportunities,” Okinawa’s total fertility rate (the estimated number of children a woman will have in her lifetime) in 2022 will be 1.70 (1.80 in the previous year), higher than the national average of 1.26 (1.30 in the previous year). In addition, the number of tourists entering Okinawa Prefecture this July, including both domestic and foreign visitors, rose 28% from the same month last year to 778,000. According to a survey by Tokyo Creative, a company that conducts business for foreign visitors to Japan, the “ranking of prefectures foreigners want to visit (March 2023 survey)” has become almost a regular occurrence, with Hokkaido in first place and Okinawa in second.

■Listed investment trusts (ETFs) called “active management type” were listed on the Tokyo Stock Exchange (TSE) for the first time on March 7. Some of them are linked to “management that is conscious of cost of capital and stock prices,” which TSE requested listed companies to do at the end of March. In particular, there is a possibility that stocks that are likely to be included in the “ETF to Promote the Elimination of P/B (Price to Book Ratio) below 1x (2080)” will be actively sought after by investors. Industries with many low P/B ratios, such as regional bank stocks, pulp and paper, construction stocks, and auto parts stocks, should be closely watched. Some stocks with high expected dividend yields, such as “NEXT FUNDS Japan High Dividend Active Exchange Traded Fund (2084)” and “MAXIS High Dividend Japan Equity Active Exchange Traded Fund (2085),” may spur speculation in high dividend yielding stocks ahead of the September mid-term ex-rights date. The market is likely to be spurred by high-dividend-yielding stocks ahead of the end of September rights.

■Toyota Motor Corp. (7203) launched its “BEV Factory,” an organization dedicated to battery EVs (electric vehicles), in May this year. Furthermore, Toyota is poised to catch up with Tesla of the U.S. and Chinese automakers that have taken the lead with its “GIGACAST” technology, which integrally molds the entire car body using aluminum die casting. If they can get on the same footing, they may be able to overtake them with the Toyota production system and the group power of their parts companies.

- 上場有価証券等のお取引の手数料は、国内株式の場合は約定代金に対して上限1.265%(消費税込)(ただし、最低手数料2,200円(消費税込))、外国株式の場合は円換算後の現地約定代金(円換算後の現地約定代金とは、現地における約定代金を当社が定める適用為替レートにより円に換算した金額をいいます。)の最大1.650%(消費税込)(ただし、対面または電話でのお取引の場合、3,300円に満たない場合は3,300円)となります。

- 上場有価証券等は、株式市況、金利水準等の変動による市場リスク、発行者等の業務や財産の状況等に変化が生じた場合の信用リスク、外国証券である場合には為替変動リスク等により損失が生じるおそれがあります。また新株予約権等が付された金融商品については、これらの権利を行使できる期間の制限等があります。

- 国内の取引所金融商品市場もしくは店頭売買有価証券市場への上場が行われず、また国内において公募、売出しが行われていない外国株式等については、我が国の金融商品取引法に基づいた発行者による企業内容の開示は行われていません。

- 金融商品ごとに手数料等及びリスクは異なりますので、お取引に際しては、当該商品等の契約締結前交付書面や目論見書又はお客様向け資料をよくお読みください。

【免責事項】

- この資料は、フィリップ証券株式会社(以下、「フィリップ証券」といいます。)が作成したものです。

- 実際の投資にあたっては、お客様ご自身の責任と判断において行うようお願いいたします。

- この資料に記載する情報は、フィリップ証券の内部で作成したか、フィリップ証券が正確且つ信頼しうると判断した情報源から入手しておりますが、その正確性又は完全性を保証したものではありません。当該情報は作成時点のものであり、市場の環境やその他の状況によって予告なく変更することがあります。この資料に記載する内容は将来の運用成果等を保証もしくは示唆するものではありません。

- この資料を入手された方は、フィリップ証券の事前の同意なく、全体または一部を複製したり、他に配布したりしないようお願いいたします。

アナリストのご紹介 フィリップ証券リサーチ部

笹木 和弘

笹木 和弘

フィリップ証券株式会社:リサーチ部長

証券会社にて、営業、トレーディング業務、海外市場に直結した先物取引や外国株取引のシステム開発・運営などに従事。その後は個人投資家や投資セミナー講師として活躍。2019年1月にフィリップ証券入社後は、米国・アセアン・日本市場にまたがり、ストラテジーからマクロ経済、個別銘柄、コモディティまで多岐にわたる分野でのレポート執筆などに精力的に従事。公益社団法人 日本証券アナリスト協会検定会員、国際公認投資アナリスト(CIIA®)。